I had an interesting conversation with someone who was asking about the mutual funds we employ. Specifically, he asked if we use “Five-star mutual funds”.

I probably shouldn’t have been surprised, based on how ubiquitous Morningstar is for investment research, but I had never been asked about Morningstar Star Ratings before.

In the world of detailed analytics and minutiae, Morningstar star ratings are a throw-away metric. It is a crude approximation of a narrow slice of a mutual fund’s story.

Morningstar is a wonderful tool for investors and advisors. The amount of data they make freely available is invaluable for the research and due diligence we perform for our clients.

However, if you don’t have a full understanding of the statistics you’re looking at, you may come to some problematic conclusions about investments.

For every mutual fund that has been in existence for three or more years, Morningstar assigns a ‘star’ rating to the fund. It appears right at the top of the webpage next to the name of a mutual fund.

Without any explanation, we can see the Morningstar star rating and assume that a fund with 1 star must be bad and a fund with five stars must be great. Here is how Morningstar defines its star ratings:

Morningstar rates mutual funds from 1 to 5 stars based on how well they’ve performed (after adjusting for risk and accounting for sales charges) in comparison to similar funds.

Within each Morningstar Category, the top 10% of funds receive 5 stars and the bottom 10% receive 1 star.

Funds are rated for up to three time periods-three-, five-, and 10-years and these ratings are combined to produce an overall rating. Funds with less than three years of history are not rated.

Ratings are objective, based entirely on a mathematical evaluation of past performance. They’re a useful tool for identifying funds worthy of further research, but shouldn’t be considered buy or sell signals.

The key is that Morningstar star ratings simply express the past performance of a fund, relative to its peers.

While we would obviously like to have been in these funds when they were outperforming, the past performance of an investment gives us no guidance toward future performance.

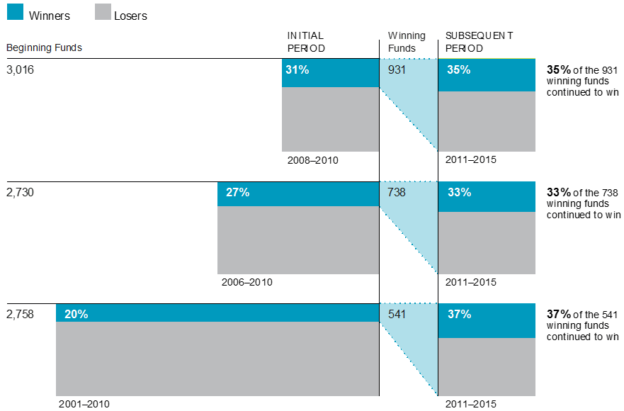

The chart below illustrates this concept. This looks at the three-, five-, and ten-year outperformance rates of equity mutual funds.

The percent of funds that outperformed their benchmarks over this period are highlighted in blue (31%, 27%, and 20%, respectively).

Of the subset of funds that outperformed, these “winning funds”, the right side of the chart takes a look at what percent of those winning funds outperformed over the subsequent five-year period.

The sample includes equity mutual funds at the beginning of the three-, five-, and 10-year periods, ending in December 2010. The graph shows the proportion of funds that outperformed and underperformed their respective benchmarks (i.e., winners and losers) during the initial periods. Winning funds were re-evaluated in the subsequent period from 2011 through 2015, with the graph showing the proportion of outperformance and underperformance among past winners. (Fund counts and percentages may not correspond due to rounding.) Past performance is no guarantee of future results. US-domiciled mutual fund data is from the CRSP Survivor-Bias-Free US Mutual Fund Database, provided by the Center for Research in Security Prices, University of Chicago.

Overall, we see that winners do not keep winning with any consistency. Indeed, in roughly two-thirds of cases, past winners have gone on to underperform their benchmarks. Vanguard put together a nice study a few years ago on the concept of “chasing returns.”

Many investors (and even advisors) who take the approach of buying five-star funds fall into a patterns of constantly buying past winners and selling losers.

This churn of always chasing what has done well in the past seems to lead to significant underperformance in the actual returns realized by investors.

So, if five-star funds aren’t what we should be buying, then what is? Three-star funds? One-star funds? Well, the answer is none of the above – or at least, we shouldn’t be looking at Morningstar star ratings at all to tell us what to buy.

We believe in a largely passive approach to investing – “buy and hold”. You can read about our investment philosophy here. In most cases, successful investing comes down to discipline.

There needs to be a certain level of acceptance for periods where your investments are underperforming. Sometimes this is a bitter pill to swallow, but chasing returns, constantly buying the five-star mutual funds, is not the answer.

Have you had trouble navigating mutual fund options or had underwhelming experiences with investing? We are happy to provide complimentary portfolio reviews.

We can show you what might not be working and strategies for positioning your assets to accomplish your goals. Give us a call or fill out the contact form on the side of this page to get started.

Once you determine that it might be time to work with a financial advisor, it’s important to find the right advisor for you and your family. We’ve put together a guide of questions that are essential to ask an advisor before you hire them.

20 Questions to Ask a Financial Advisor

Don’t make a mistake by working with the wrong financial advisor. Ask the right questions the first time to determine if a financial advisor is right for you.

If you’re looking for a wealth manager and financial advisor that puts you first, call Ferguson-Johnson Wealth Management today!

CONTACT US