Let’s talk about bonds for a minute. Occasionally, we get asked about what the future prospects are for bond investors. Sometimes with the implication being: “Should I be invested in bonds at all?” For the past decade, we’ve lived in a very low interest rate environment, relative to historical averages. (Click charts below to enlarge)

10-Year Treasury Yields Over Time

Source: Yahoo Finance, as of 3/21/2018

For a lot of good reasons, interest rates are near all-time lows right now. Bonds currently pay little in interest to their investors, which has made planning for retirement more challenging for retirees and investors with shorter investment time horizons. Looking forward, we expect that at some point interest rates will rise.

Indeed, the Federal Reserve has made several moves in the past year to bring interest rates up slightly from their all-time lows. However, forecasting the when, the magnitude, and even the direction of interest rates would be foolish.

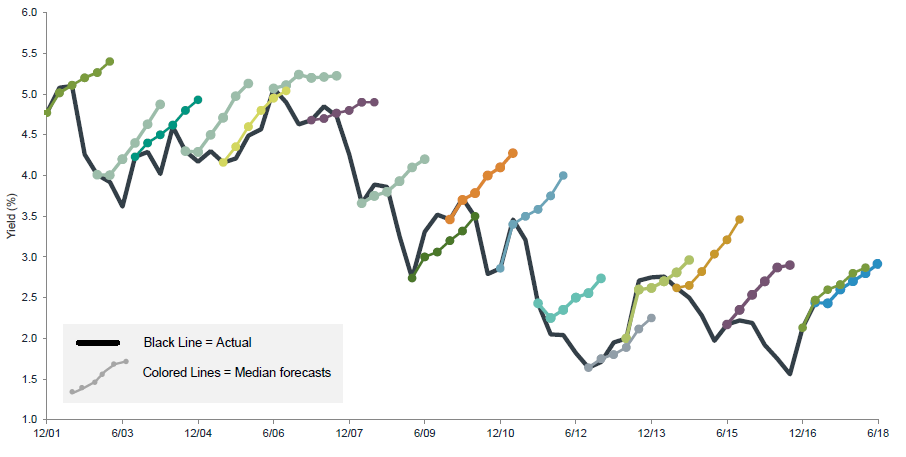

The chart below illustrates professional economic forecasters’ aggregate predictions of where they believe interest rates would move over subsequent short periods. The results reveal that the even the professionals have been laughably inaccurate.

10-Year Treasury Rate – Median Forecast vs. Actual

Source: Federal Reserve Bank of Philadelphia, as of 3/31/2017. The black line represents the actual rolling 10-year note yield while the colored lines represent forecasted numbers. Each colored line represents rolling 5-quarter forecasts by the professional forecasters (median).

Before we go any further, we need to be clear on one of the core aspects of fixed income investing – The inverse relationship of bond prices and interest rates. As interest rates rise, the price of existing bonds fall, and vice-versa. This concept is very unintuitive to uninitiated investors. So, let me try to explain why this is the case.

Most bonds have fixed coupon payments. Which is to say a bond providing 4% interest will provide the same 4% level of interest to the bondholder at all points in its life-cycle. The interest it pays does not adjust to changes in prevailing, market interest rates.

This is important because how valuable a bond is will change depending on how market interest rates move. Let’s look at an example:

An investor purchases a five-year bond paying 4% interest for $100. The prevailing interest rate in the market at this time is also 4%. After one year, that bond has provided the investor with $4 of interest and now has four years remaining until maturity.

However, over the past year, the market interest rate of similar bonds rose to 5%. Therefore, new bonds are being issued that pay 5% interest to investors. These 5% interest bonds still cost $100 (and repay $100 at maturity), as the bond our investor purchased last year did.

The investor decides they want get rid of the bond they purchased a year ago, but this raises an issue. Who would want to buy a bond that pays 4% when they can go out and get a bond that pays 5% for the same price? The answer is no one.

So, if the investor wants to sell his bond, it needs to be priced at a discount (in this case, $96.45 in order to provide an equivalent yield to the new bond).

Notice that in this scenario, the investor’s absolute return is still positive (gain of $4 of interest, loss of $3.55 on sale = net return of $0.45). Not a stupendous return, obviously, but – Hey, at least its positive.

Also note that this represents a pretty dramatic spike in interest rates – a one percent increase over a one-year period. A smaller increase, or an increase extended over a longer period of time, would result in a reduced loss of principal.

As we illustrated, rising interest rates can reduce the nominal price of bonds. This results in one dimension of the returns produced by bonds to be negative. However, it is important to bear in mind that these existing bonds are still paying interest to their holders, irrespective of changing interest rates.

These interest payments, in most cases, make up the overwhelming share of returns attributable to a fixed income investment. Furthermore, in a rising-rate environment, as those interest payments come in, they can be reinvested into higher interest-paying bonds. This reinvestment will gradually increase the return an investor earns on those investments (holding other factors constant).

For investors that have longer investment time horizons, this is good news! Languishing in a low interest rate environment indefinitely would endanger the investment return assumptions that are likely necessary to successfully accomplish financial goals.

For many investors who are saving for longer-term goals, the purpose of bonds in a portfolio typically is not to provide absolute return. Instead, the primary role of fixed income is to serve as a volatility hedge to the equity portion of a portfolio.

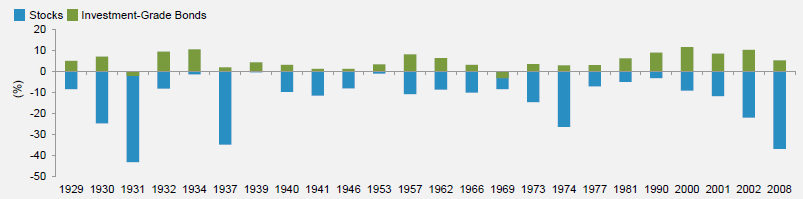

Historically, when equity markets experience drawdowns, high-quality fixed income investments have often carried a negative correlation to those equities. This resulted in the fixed income portion of a portfolio offsetting some of the losses on the equity side.

Fixed Income Performance When S&P 500 Declines

Source: Morningstar EnCorr and Fidelity Asset Allocation Research Team (AART), as of 12/31/16. Investment-grade bond returns are represented by the BBgBarc U.S. Aggregate Bond Index from January 1976 and by a composite of the IA SBBI U.S. Intermediate-Term Government Bond Index (67%) and the IA SBBI U.S. Long-Term Corporate Bond Index (33%) from January 1926 through December 1975. Stock returns are represented by the performance of the S&P 500 Index.

Given that financial capital needs to be allocated somewhere, the reasonable options, for most investors, are equity, fixed income, and cash. If one were to choose to avoid fixed income investments for fear of rising rates, we’re left with two options that pose potential problems.

Additional equity investment would significantly increase the risk of an investor’s portfolio which would likely be unsuitable. On the other hand, cash provides a negative expected real return. Fixed income, in a rising rate environment still provides an expected positive return – unless the rise is both large and quick. For a balanced portfolio, investors shouldn’t fear fixed income.

If you’re looking for a wealth manager and financial advisor that puts you first, call Ferguson-Johnson Wealth Management today!

CONTACT US