One question that seems to be popping a lot is “Why aren’t stocks down more?” After all, we’re in the midst of what I hope will be the worst economic calamity of this generation and equity losses are only moderate as we sit here today.

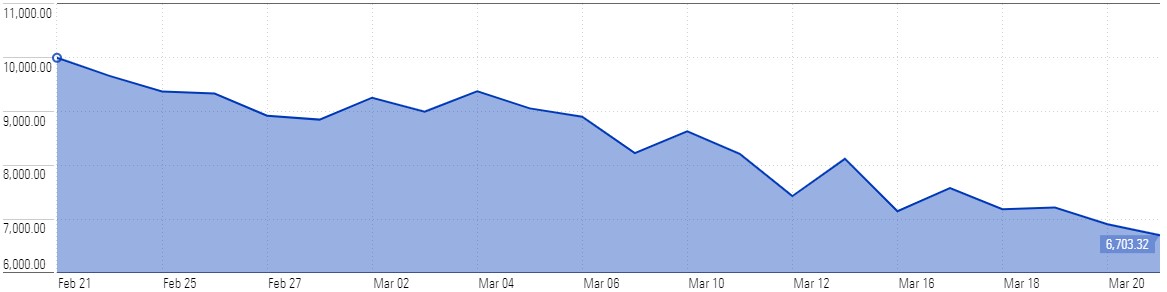

I have a few ideas as to why markets aren’t in worse shape. But first, let’s look at the path the US stock market has taken from the beginning of all this up until now. From February 21st through March 23rd, the S&P 500 fell 33%.

S&P 500. Growth of $10,000, 2/21/2020 to 3/23/2020. Source: Morningstar.

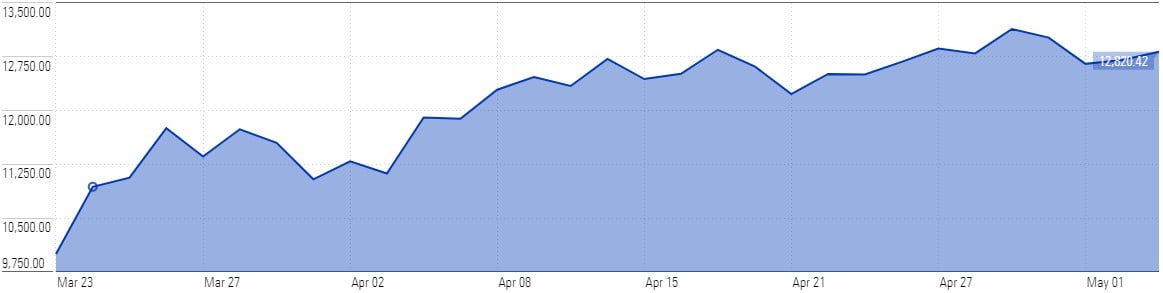

From there, markets have risen 28%, from the low on March 23rd.

S&P 500. Growth of $10,000, 3/24/2020 to 5/3/2020. Source: Morningstar.

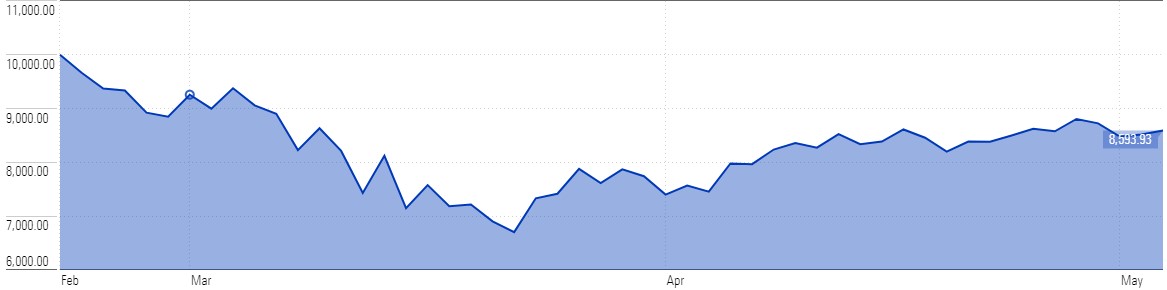

Overall, we can observe that since the COVID-19 crisis began, domestic markets are down about 14% from their February highs.

S&P 500. Growth of $10,000, 2/21/2020 to 5/3/2020. Source: Morningstar.

A bad couple of months, to be sure. But, not too terrible in the context of market declines we’ve seen before.

I write this as a sit in one of two makeshift offices my wife and I have cobbled together. The one I seem to be using most often happens to also be our cat’s litter room. I can look out the window and see that the parking spaces in front of my neighbors’ homes are nearly all filled – It’s 11:00am on a Thursday.

Last weekend, I stood on a piece of tape behind about 20 other people (each on their own piece of tape, six-feet apart) for about 40 minutes waiting to enter my local grocery store.

They didn’t have any flour. As I read the news today, the Wall Street Journal informs me that 33.5 million people have filed unemployment claims since the beginning of March. A couple weeks ago, the price of oil was negative.

Things are not ideal. So, what gives? Why is the market not down more? Let me throw out a few theories that could partially explain the overall resilience of equity markets in the face of Coronavirus.

Let’s not forget what stocks are at the end of the day. A stock is a piece of ownership in a company entitling the owner to a share of the future earnings of that company. While earnings may be low, zero, or negative in the coming months, your claim on the company’s future earnings is still there.

This ownership entitles you to the earnings that company produces a year from now, a decade from now, and beyond. In the grand scheme of things, it may not matter if there is a bad quarter or year.

Obviously, to see your share of those earnings come through in the future, the company must stay in business. Inevitably, this crisis will probably drive some companies to bankruptcy.

But, I would assume that most companies will still be around once this hardship passes. For the majority of businesses not in the cruise line industry, I think this is a relatively safe assumption.

A few months from now, or a few years from now, or whenever your personal belief about when things will return to normal happen to be, people will probably still buy iPhones and take vacations.

So long as people are willing to spend money on goods and services, there will be economic growth and profits for companies to realize and pass along to shareholders.

Another simple explanation for why stocks aren’t lower might be answered by the question: Where are you going to go? During past market declines, fixed income offered investors attractive yields as an alternative to the riskiness of equities.

When investors grew fearful, they were able to flee into bonds where they could earn reasonable interest and ‘weather the storm’.

If we look back to the 1980s, annualized returns for holding 3-month treasury bonds oscillated between 5-14%. Today, FRED data shows that same bond yielding 0.13%. An investor in 1984 could have thought “you know, I just can’t stomach the volatility in stocks right now, I’ll just settle with the 9% I’ll earn on T-bills for right now.”

Investors today do not have that luxury. It may just be that investors can’t afford not to be in stocks for the sake of their financial goals.

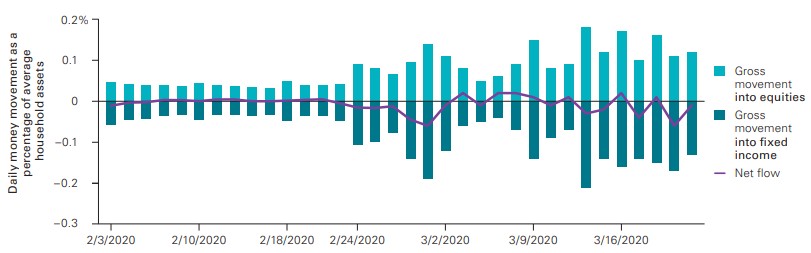

Perhaps related to my theory above, it appears the overwhelming majority of investors have not been fleeing from equities to cash or fixed income.

According to Vanguard, while overall trading activity has risen, only 9.3% of investors with at least one Vanguard account made a trade between February 19 and March 20. If we dig into their data bit further, we can see that a little less than half of that trading activity has been money flow into equities.

Vanguard US household assets have moved modestly into fixed income. 2/3/20 to 3/20/20. Source: Vanguard

We can quibble about the efficiency and targeting of the governments stimulus efforts, but the sheer nominal value of aid being made available to individuals and business is staggering.

According to the Committee for a Responsible Federal Budget figures, to date, $3.6 trillion of fiscal support has been authorized to support the US economy. This is a massive number and it seems to be helping.

The small business loans have staved off more significant layoffs at many companies and for low-to-mid income workers that have lost jobs, unemployment benefits are replacing 100% or more of their lost income.

As I’ve said before, I don’t know how anything will unfold from here. Anyone who does is either outright lying with some agenda or they are delusional. I would not be surprised if we revisit the lows from March, nor would I be surprised if markets begin hitting new all-time highs by summertime.

Because the stock market seems to be so good at making fools out of anyone with enough hubris to think they know what’s next, I believe it is more important than ever to revisit the appropriateness of an investment plan.

Is there too much risk in your portfolio? Too little? We use a tool to help quantify risk tolerance.

If you’re looking for a wealth manager and financial advisor that puts you first, call Ferguson-Johnson Wealth Management today!

CONTACT US