It’s Required Minimum Distribution (RMD) season (or Minimum Required Distribution – MRD, same thing). Beginning the year an individual turns 70 ½ mandatory distributions from certain tax-deferred retirement accounts must begin.

Each year, the amount required to be distributed increases as a percentage of a retirement account’s balance. This percentage starts out small – about 3.5% of the account’s value – and increases to nearly 10% of the account value by age 92 (and continues to increase beyond that). You can find the full distribution table at the IRS website.

The rationale behind RMDs is simple. The federal government has allowed individuals to take a tax deduction on contributions to retirement accounts while working. Now they would like to receive some tax revenue on those deferred monies.

The penalty for failing to take your RMD is severe. The IRS imposes a massive 50% penalty on the amount of an undistributed RMD.

So, if your RMD was $30,000 for the year and you failed to take at least that amount from your accounts by December 31st, the IRS will be sending you a bill for $15,000. Obviously, it is imperative that you be on top of RMDs in order to avoid this penalty.

Importantly, if you are already taking distributions from your retirement accounts for your living expenses, you may not have to withdraw any additional retirement money to satisfy your RMD.

Remember – RMDs are required minimum distributions. If you require cash flow for living needs in excess of your required amount for the year, then the RMD itself is moot.

If you are of RMD age, you must take RMDs from your tax-deferred retirement accounts with little exception. However, if you are still working and recognizing earned income from an employer, you are not required to make RMDs from retirement accounts sponsored by that employer.

Although, you would still need to take an RMD from IRAs or other retirement accounts held away from your employer.

Generally, RMDs are calculated on a per account basis. So, if you have multiple IRAs, 401(k)s, and other accounts, your financial advisor or account custodian will determine the amount necessary to be withdrawn for each account, individually.

For certain accounts, you are permitted to combine the RMD total and take the distribution from just one account.

This applies to IRA accounts (Traditional, SIMPLE, and SEP) and 403(b) accounts. So, if you have an IRA at Fidelity and an IRA at Schwab, you could add up the total RMD and take the distribution from just the Schwab account, if you so choose.

This exception does not apply to a 401(k)’s. If you happen to have multiple 401(k)’s, you must take the full required amount attributable to each account from the account itself.

We often get asked: “When should I take my RMD – at the beginning of the year or the end?” On the assumption that this RMD is not reinvested in a taxable account, the answer to this question isn’t entirely satisfying. We can only know the correct answer in hindsight.

If your portfolio happens to decline in a given year, then it would have been better to take an RMD at the beginning of that year. The opposite would be true if your investments gained in the year. It’s impossible to know ahead of time what the ideal course of action will be.

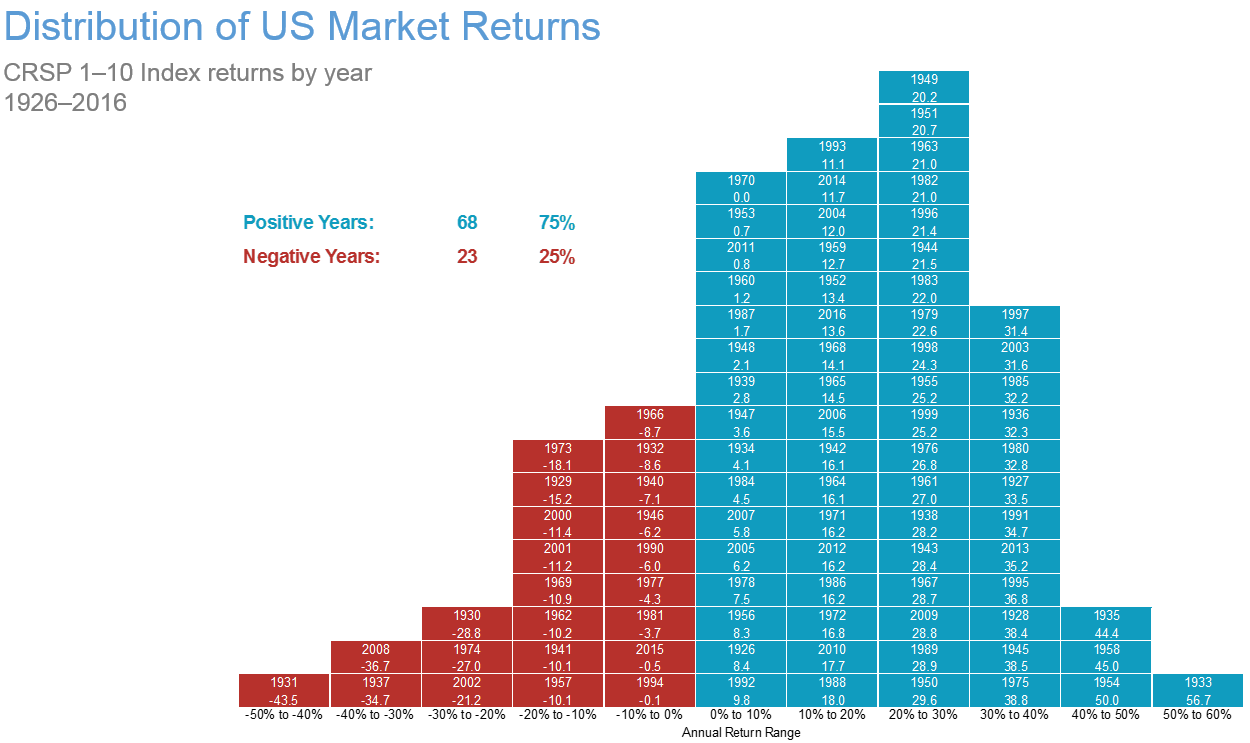

Below is a chart of the US stock market’s annual distribution of returns. In the majority of years, stocks provide a positive return. Therefore, in the majority of years, it probably would have been better to leave your funds invested for most of the year.

Investors that get too worked up over the possibility of choosing wrong can employ a monthly distribution aimed to dollar-cost average the RMD out of their accounts over the course of the year. This also can operate as a sort of ‘paycheck’ to the RMD recipient (for those that need the RMD money for expenses).

RMDs can pose a tax burden on retirees. For families that derive significant income from non-retirement account sources, such as Social Security, pensions, rental income, or taxable investment assets, the extra, unneeded income required to be realized from IRAs and 401(k)’s can result in taxation at high, undesirable rates.

For savers that are still working, or enjoying their early years of retirement, there are planning strategies that can be employed to help mitigate the eventual tax burden of RMDs.

Unfortunately, once an individual has already reached RMD age, the options for managing the tax consequences of RMDs are somewhat limited, but there are still some tools available.

One approach that has become increasingly popular is making a Qualified Charitable Distribution (QCD) directly from an IRA in the amount of an RMD. This will allow the entire distribution to avoid being reported as taxable income, thus avoiding the tax burden created by the unneeded RMD.

While this may sound like a potentially effective strategy (and in many cases, it is!), it is important to note that it may be more advantageous to make charitable contributions from highly appreciated taxable assets instead.

If you are already itemizing your deductions (before any charitable contributions are made). You may be better off donating appreciated assets from a regular, taxable account that you would otherwise need to pay capital gains tax for selling. In this case, it would likely be better to take the RMD normally and pay the applicable tax.

Keep in mind, a QCD or the tax benefits of regular charitable gifting are only beneficial to the donor to the extent that they were already planning to make charitable donations.

For those that don’t actually plan to make charitable donations, from a financial standpoint, you better off paying taxes and keeping the remainder. Before acting on a Qualified Charitable Distribution strategy, you should talk things over with your financial and/or tax advisor to determine the most effective course of action.

I could write an entire blog post, and then some, on considerations at play for implementing a Roth Conversion strategy. The general idea, concerning RMD tax mitigation, is to reduce the balance of traditional retirement accounts by way of converting portions of those accounts into Roth accounts. This would have the effect of lowering your eventual RMDs and the tax bill that goes along with them.

Furthermore, by offsetting the portions of realized income in retirement, it may be possible to reduce premiums for Medicare or even the taxability of Social Security payments.

To take a small step back, the primary decision to contribute assets to a traditional or Roth account is based on the assumption that your tax rate today will be different than it will be when you draw on retirement assets.

If you expect your future marginal tax rate to be greater than it is today, Roth contributions are generally a more effective saving strategy. If you expect your marginal tax rate to be lower when the time to take distributions comes, then contributions to traditional accounts are generally more effective.

Potential tax reform throws a wrench into these considerations as well. Under proposed legislation, many families, at all income levels, may see their marginal tax rate decline. If such legislation passes, it may look foolish to have made Roth conversions in the past few years.

Unfortunately, the nuanced details specific to an individual’s situation and their expectations about the future are ultimately going to dictate the viability of a Roth Conversions strategy. So, it would be unwise to simply make a decisions to pursue a conversion strategy based on what you read in a blog post. Please consult your financial advisor before attempting a Roth Conversions strategy.

For a working couple, if resources do not allow for maximum contributions to both spouses’ retirement accounts while working, it may be advantageous to max-fund the younger spouse’s account first.

After both spouses contribute enough necessary to take full advantage of any matching or bonus contributions, the younger spouse would then fill up their contribution bucket before further funding the older spouse.

The result of this action is that the younger spouse ends up with the larger tax-deferred retirement account. This delays the RMD applicable to the couple, on a per-dollar basis, further into the future.

The corollary to this strategy is doing the inverse when it comes to distributions from retirement accounts. When income needs arise in retirement, it may be advantageous to take distributions from the older spouse’s account.

This has the same effect as overweighting the younger spouse’s contributions as noted above – shrinking the older spouse’s tax-deferred assets and expanding the younger spouse’s.

The mileage of these strategies is going to depend on how large the age-gap is between spouses. The greater the age difference, the more material this strategy may be.

There are numerous other strategies that may apply to niche situations, such as splitting assets strategically in a divorce or 401(k) roll-ups. Ultimately, it’s important to understand that the tax obligations of tax-deferred accounts can’t be avoided completely.

However, it is possible to manage and plan for the onset of those taxes. By minimizing the size of RMDs, it can be possible to take advantage of further tax-deferred growth.

Once you determine that it might be time to work with a financial advisor, it’s important to find the right advisor for you and your family. We’ve put together a guide of questions that are essential to ask an advisor before you hire them.

20 Questions to Ask a Financial Advisor

Don’t make a mistake by working with the wrong financial advisor. Ask the right questions the first time to determine if a financial advisor is right for you.

If you’re looking for a wealth manager and financial advisor that puts you first, call Ferguson-Johnson Wealth Management today!

CONTACT US